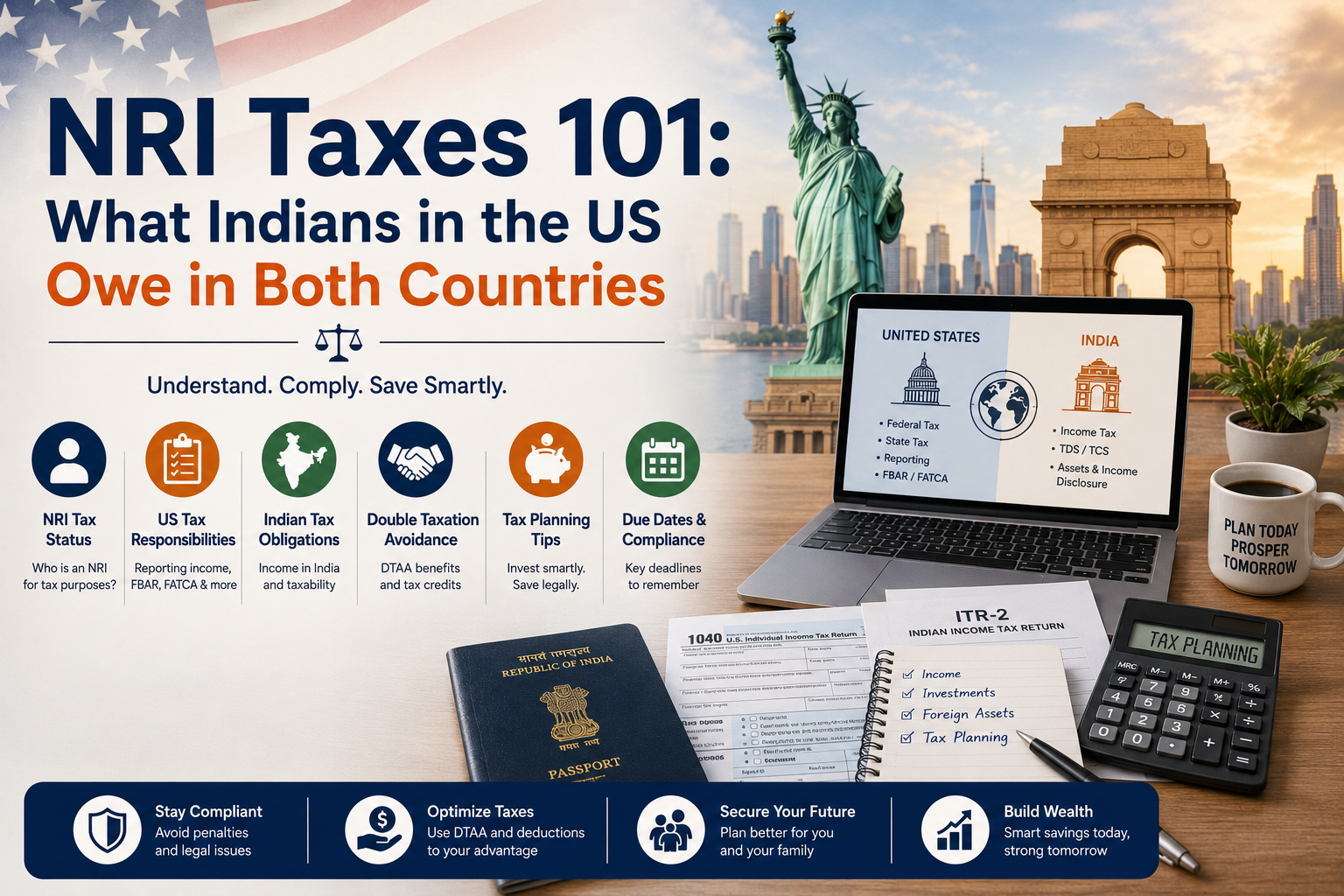

NRI Taxes 101: What Indians in the US Owe in Both Countries

NRI Guide desk

NRI Herald • July 12, 2026

3 min read

Living in the United States while keeping money and family ties in India puts you under two tax systems at once. This is a plain-English map of how they fit together. It is general information, not tax advice; a cross-border situation deserves a qualified professional.

The United States taxes its residents on worldwide income. If you are a US tax resident, whether by citizenship, a green card, or the substantial-presence day-count test, you report income earned anywhere on your US return, including Indian salary, rent, interest and capital gains.

India taxes you based on residency under its Income Tax Act. Broadly, if you spend fewer than 182 days in India in a year, subject to some finer tests, you are a Non-Resident Indian, and India taxes only your India-sourced income: salary earned in India, rent from Indian property, interest on certain accounts, and Indian capital gains. Global income is generally outside India's net for a clear NRI.

NRIs typically use special bank accounts, and the difference matters. Interest on an NRE account, funded from foreign earnings and fully repatriable, is generally exempt from Indian tax. Interest on an NRO account, funded from India-based income, is taxable in India and often has tax deducted at source. Both, however, are reportable on the US side if you are a US tax resident.

Two US disclosure rules trip up many NRIs:

These are information forms, but the penalties for failing to file can be steep even when no extra tax is owed.

The India-US tax treaty and the US foreign tax credit exist so that the same income is not fully taxed twice. In practice, if you pay Indian tax on Indian income, you can usually claim a credit against the US tax on that same income, and the reverse can apply too. The mechanics are technical and are worth professional help to get right.

For most Indian professionals in the US, the rule of thumb is this: the US wants to see your worldwide income and your foreign accounts, while India taxes what you earn in India. Getting the overlap right, the credits, the disclosures and the account types, is where a cross-border accountant earns the fee. Confirm current thresholds and rules with a professional and with the official IRS and Indian Income Tax Department sources before you file.

Highlighted words show why each story was matched

NRI Herald • July 12, 2026

NRI Herald • July 12, 2026

NRI Herald • July 12, 2026

NRI Herald • July 12, 2026