Sending Money From the US to India: A Practical Guide for NRIs

NRI Guide desk

NRI Herald • July 12, 2026

3 min read

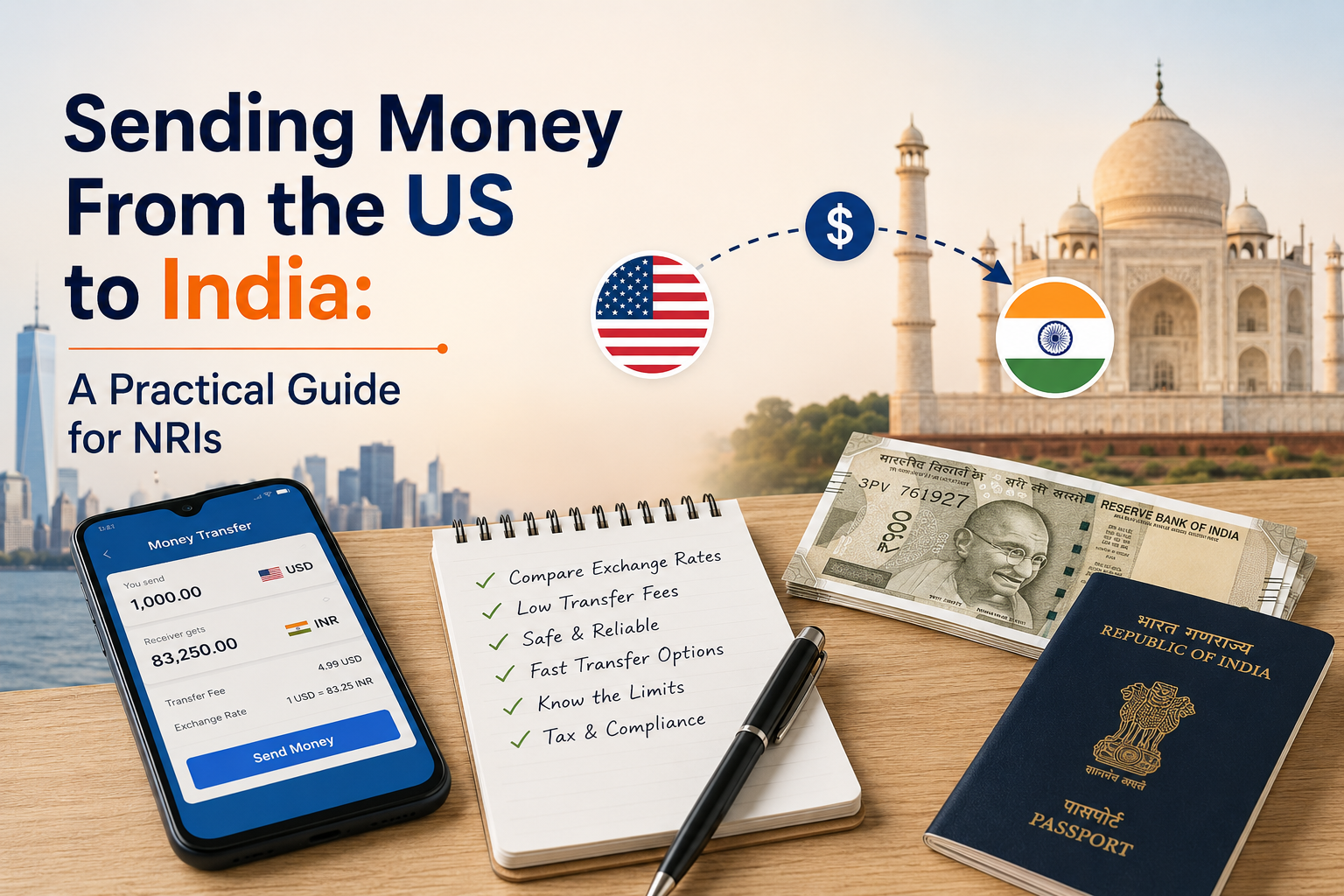

Sending money home is something almost every NRI does, and small differences in how you do it add up fast on a large transfer. The goal is simple: get the most rupees to the right account, cleanly and on record. Here is how to think about it. This is general information, not financial or tax advice.

The exchange rate and the fees together decide how many rupees actually land. A headline offer of zero fee can still cost you if the rate is poor. Always compare the total rupees received, not just the advertised fee.

Look at the all-in cost: the rate you are offered versus the mid-market rate (the gap between them is the spread), plus any flat fee. Two services with the same fee can deliver very different rupee amounts because of the spread.

Pick the method with the best all-in rate for the amount you are sending, use the right receiving account, and keep clean records. Confirm current tax thresholds with a professional and the official IRS and Indian Income Tax Department sources.

Highlighted words show why each story was matched

NRI Herald • July 12, 2026

NRI Herald • July 12, 2026

NRI Herald • July 12, 2026

NRI Herald • July 12, 2026